"What gets measured gets managed." A critical part of the Retirement Income Covenant requires that trustees establish metrics to measure the effectiveness of their retirement income strategies. When it comes to Retirement, these metrics are typically very different from what we see in the accumulation space, with some useful examples being shared by the regulators:

- Modelling the range of likely outcomes for members

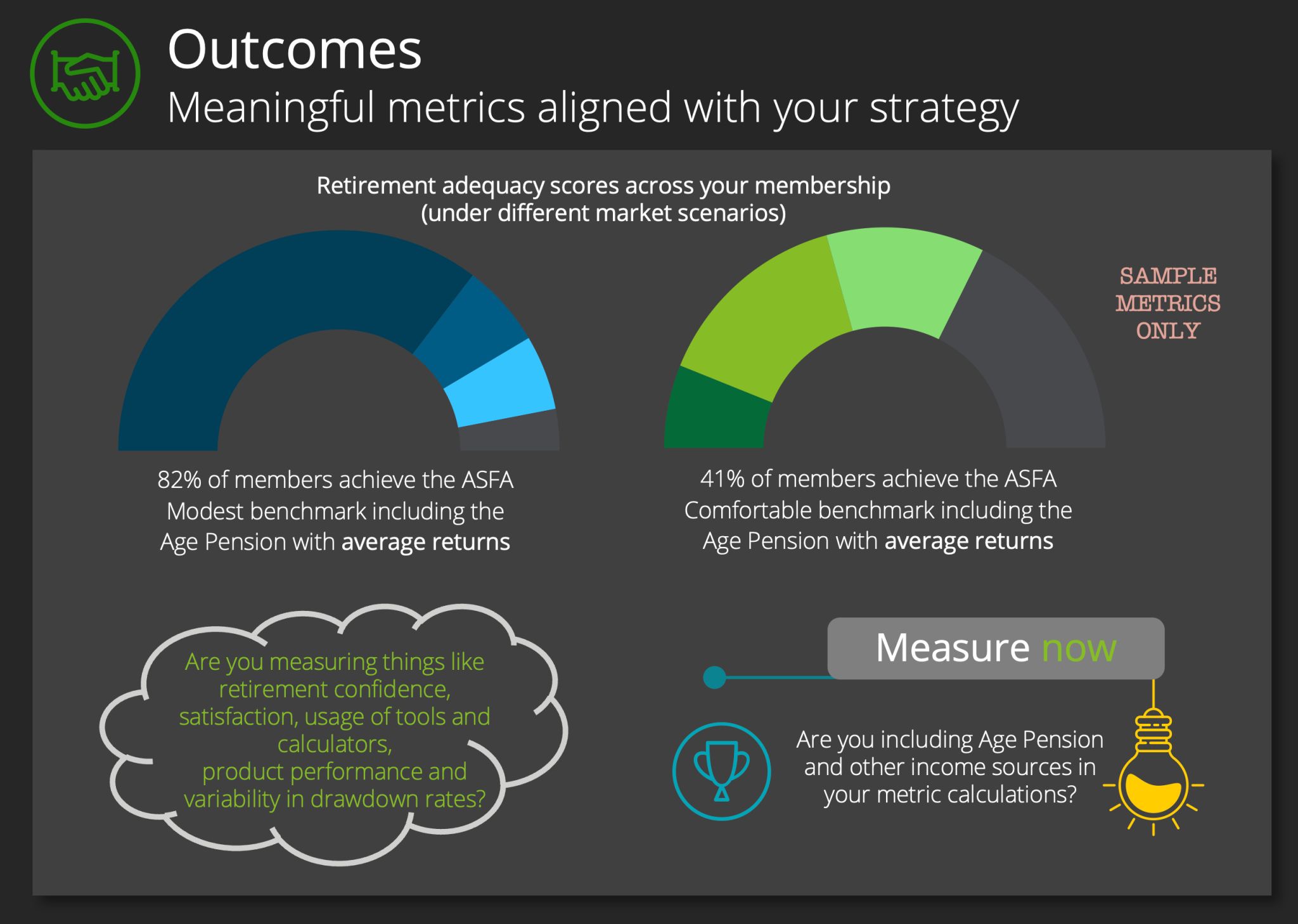

- Proportion of members meeting retirement adequacy measures

- Actual drawdown amounts against estimates

- Engagement scores for members approaching and in retirement

- Differences in the take-up of assistance offered between advised and unadvised members

- Retirement confidence of members in drawdown phase

- Remaining balances after members pass away

- Conversion rate of accumulation accounts into retirement income products

Modelling many of these metrics can be a complex exercise, especially when seeking to understand the range of probabilistic outcomes across your membership – and not merely the average.

"We don't get to live out a thousand retirements and take the average outcome."

Regardless of what set of metrics you put in place, the important thing is that they are not merely set up for the sake of having them, but rather they act as a catalyst for you to revisit your strategy based on what the metrics are telling you.

I'll see you at the Australian Financial Review Super & Wealth Summit to discuss the above and more. Limited tickets left, join Deloitte on October 29.