In moving from a DB to a DC retirement savings system, we have effectively delegated a lot of complex decisions to the individual. This is problematic when we consider that most retirees do not have a good understanding of our retirement system and its risks, do not seek independent financial advice, and apathy abounds when it comes to superannuation.

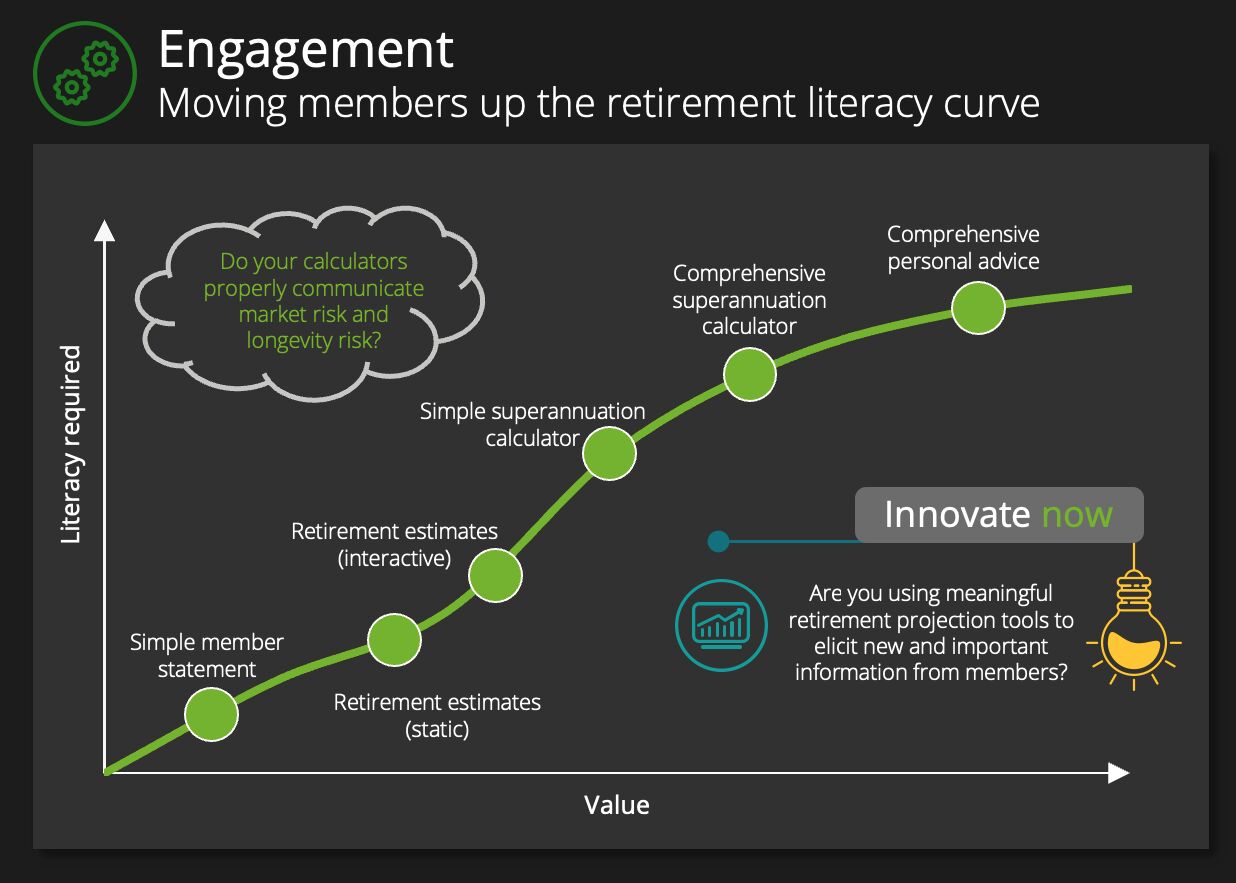

The challenge for super funds is to find a way to engage their members with superannuation, particularly as they approach retirement, and somehow move them up the "retirement literacy" curve. This challenge becomes even more difficult once we recognise that there is a wide distribution of retirement literacy levels across and within funds, and no matter how good your shiny new calculator is, if your members do not understand simple super concepts, they aren't going to reap the full benefits of your digital engagement strategy.

The good news is there are plenty of tools available to help funds do this, starting with the very basics. For example:

- Have you made an assessment of the level of retirement literacy across your fund membership?

- Do all of your members understand their annual statement?

- Are you taking advantage of ASIC Instrument 2022/603 and RG 276 to provide an interactive retirement estimate to members, using information you already know about them?

- Do you have a comprehensive set of digital tools that complement each other and consistently present information back to your members, or do you need to build out a roadmap for such a suite of tools?

- Do your superannuation calculators accurately and intuitively display investment and longevity risk in a way that is easy to understand?

- Are you making your digital experience so useful to your members such that they actively wish to engage with your calculators and provide you with additional information about their circumstances that you can use later on to further customise your offering and ultimately provide hyper-personalised experiences?

- Does your help, guidance and advice offer leverage your established suite of digital tools and the information you have collected from them?

All of the above can be done today, regardless of what legislation comes out of the Quality of Advice Review consultation process. In fact, funds that have set up the above infrastructure are expected to be the early movers on any legislation promoting an increase in scaled advice.

I'll see you at the Australian Financial Review Super & Wealth Summit to discuss the above and more.