Having specific "Retirement" teams (sometimes with an executive leader) has become the norm for super funds in recent years, but what exactly is Retirement anyway and isn't the whole purpose of superannuation to help members save for and access their savings in retirement – so why do we need a separate team?

Well, on 1 July 2022, things changed with the advent of the Retirement Income Covenant, which – although principles-based – placed an obligation on trustees to develop and implement a Retirement Income Strategy for their members approaching and in retirement. This strategy is quite broad in scope and covers all kinds of areas, such as investigating members analytically with the data trustees have on hand, the approach to education, assistance and guidance, as well as product. On top of that, the Retirement Income Strategy needs to be consistent with other initiatives at the fund (including those governed by SPS 515), and outcomes against the strategy need to be reviewed regularly. So quite clearly a large obligation for trustees to fulfil.

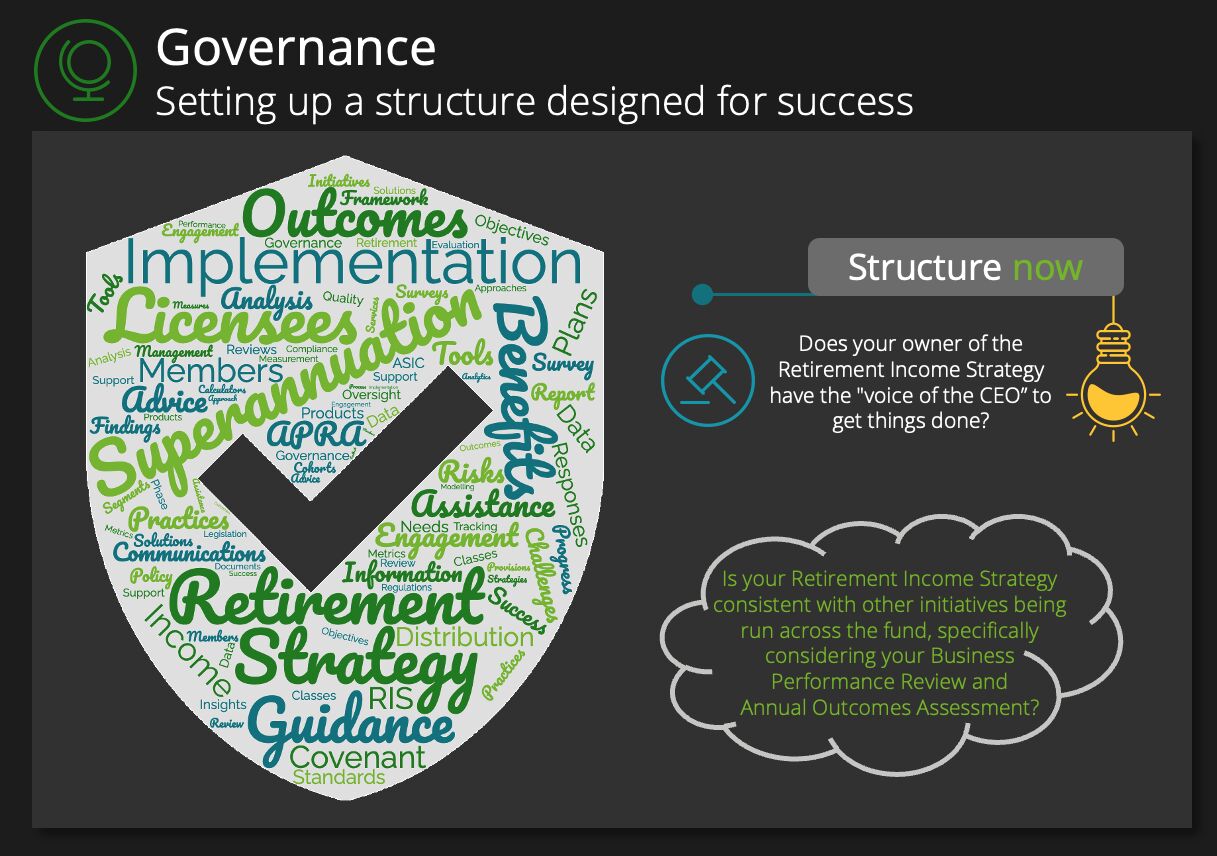

This leaves us with two practical questions for funds to consider:

- Does your owner of the Retirement Income Strategy have the "voice of the CEO" to get things done – or do you simply have a theoretical strategy that loses in priority to other fund initiatives?

- Is your Retirement Income Strategy consistent with other initiatives being run across the fund, specifically considering your Business Performance Review and Annual Outcomes Assessment – or are you finding yourself competing with other internal teams based on different KPIs and measures of success?

Funds that can answer positively to the above questions are well-placed to implement their Retirement Income Strategy efficiently and will be the first to demonstrate to the regulators the "step change" they are expecting.

To quote ASIC Commissioner Simone Constant: "It's about being accountable to your member, from the trustee board down. For this to occur, you need the right people, at the right levels, who are empowered to make good member and good retirement outcomes a priority."