In Australia's current retirement landscape, super funds are being encouraged to develop trustee-designed retirement solutions - thoughtfully crafted combinations of account-based pensions, emerging lifetime income products, and the Age Pension - to deliver more reliable, sustainable income for different cohorts of members. Yet in practice, most retirees manage these elements independently, applying for the Age Pension themselves, handling ongoing disclosures to Services Australia, and drawing down super in ways that often lead to volatile or suboptimal outcomes. The result? Income that feels more like a bumpy ride than the steady paycheck many enjoyed during their working years.

A streamlined "retirement paycheck" - where the fund automates Age Pension applications, dynamically adjusts drawdowns, and provides consistent, inflation-adjusted payments - could bridge this gap. Here's why it matters and how the current reality falls short.

What exactly are trustee-designed retirement solutions and why do they matter?

According to Treasury, trustee-designed solutions are "retirement income solutions designed by the trustee for its identified retiree cohorts, with consideration for the financial characteristics and preferences of the members within those cohorts". This means they are effectively personalised drawdown strategies created by super fund trustees, integrating account-based pensions, lifetime income options, and Age Pension support, tailored to factors like age, balance, and preferences for risk, flexibility and income level.

In this way, they directly support the Retirement Income Covenant obligations of the trustee, by helping members navigate the trade-off between the retirement trilemma: maximising expected retirement income, managing risks associated with the stability and sustainability of that income, and maintaining flexible access to expected funds in retirement. With the total assets in the drawdown phase of super alone approaching $4 trillion over the next 20 years, these guided approaches can boost confidence and reduce the fear of outliving savings for many Australians. The challenge lies in moving from theoretical designs to practical delivery.

The current reality: navigating Age Pension and disclosures alone

Applying for the Age Pension is a DIY task for most: submitting detailed income, asset, and residency information via myGov, then complying with ongoing Department of Social Services (DSS) disclosure rules, by providing information to Services Australia in a timely manner, to avoid underpayments or penalties. Without fund support, errors are common, entitlements get missed, and drawdowns often misalign with actual Age Pension payments - undermining the integrated outcomes trustee-designed solutions aim to achieve.

The bumpy road of account-based pensions

Retirement cash flow, which is most commonly delivered through a combination of the means tested Age Pension and an account-based pension, rarely mirrors a predictable salary. Market volatility, combined with compulsory minimum drawdowns (starting at 4–5% for ages 60–74 and rising to 14% by age 95), creates unpredictable withdrawals - higher in good years, strained in bad ones, and increasing over time - counterintuitively providing retirees with less income during the more active phase of their retirement, and often leaving significant capital remaining upon death. Many retirees play it safe and underspend to preserve capital, sacrificing dignity and standard of living, or draw too aggressively and risk early depletion. This instability, without many guardrails, highlights the need for better smoothing.

The rise of lifetime income solutions: a third pillar takes shape

Lifetime income products are gaining momentum to counter longevity risk, providing guaranteed or investment-linked payments for life. Already, a handful of super funds offer these products, with more on the way. They form a stable third income source alongside account-based pensions and the Age Pension, potentially offering a reliable baseline in volatile markets, that can last well beyond life expectancy.

As policy support and targeted distribution uplift across funds drive greater adoption, this three-pillar approach is positioned to be the baseline. Coordinating the pillars, however, remains complex without seamless integration. That is to say, there is little point as a fund in developing trustee-designed solutions if there is no mechanism in place to deliver them as planned.

A worked example: typical reality vs trustee-design ideal

Consider a single 67-year-old retiree with a $600,000 super balance, using 80% to start an account-based pension in 2026 (minimum drawdown rate: 5%). They have also taken up their fund's trustee-designed solution for them that involves 20% of their super balance ($120,000) being placed into a guaranteed annuity. Note that this trustee-designed solution was constructed by assuming theoretical market and drawdown experience that results in flat real income over time.

In practice, however, the income profile can look very different...

In reality, retirement income is a bumpy ride!

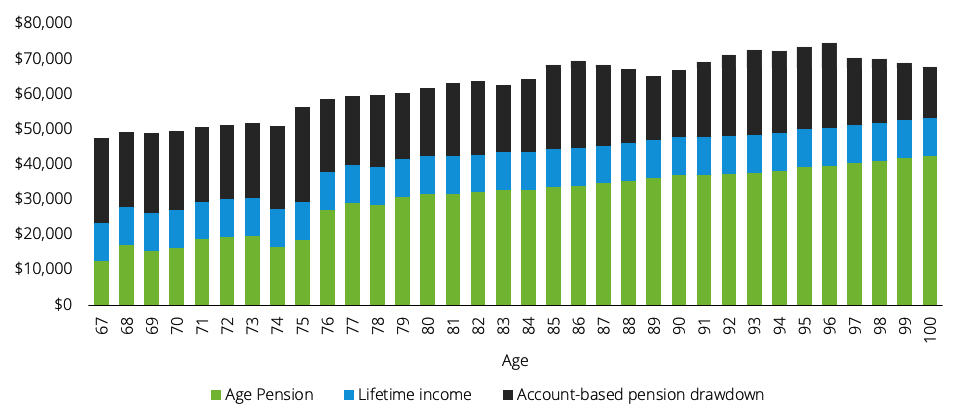

Typical reality (suboptimal): The retiree draws only the minimum $24,000 annually from the account-based pension and manages the Age Pension application and disclosures independently. Investment returns fluctuate (e.g., strong one year, weak the next), Age Pension payments adjust irregularly based on deeming rules and disclosures, and as a result cash flow varies significantly. Over time, as the retiree becomes entitled to more Age Pension, income increases in the more passive phase of retirement.

Result: Income swings between $47,000–$74,000+ (including partial Age Pension), with periods of caution or shortfall, and potential missed optimisation of entitlements, particularly in the earlier years of retirement.

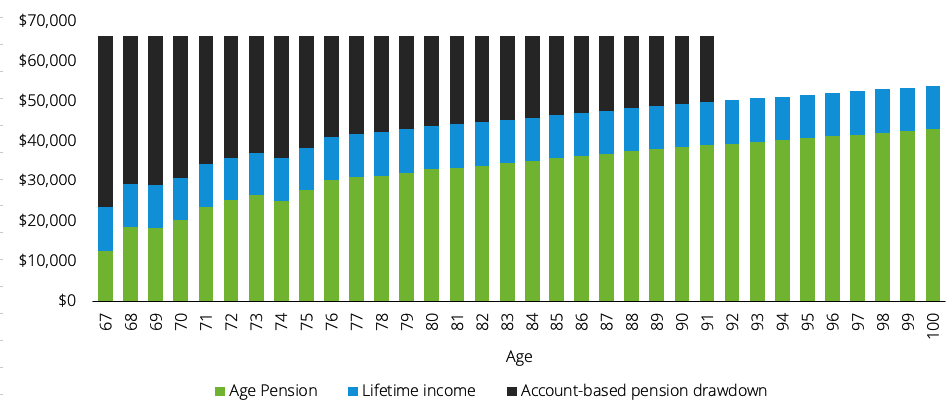

Trustee-designed ideal (with retirement paycheck): The fund acts as an agent of the member and applies for the Age Pension on the member's behalf, and drawdowns adjust automatically to target a smooth $66,000 total real annual income (inflation-adjusted) to life expectancy, optimising social security, preserving entitlements longer, and smoothing volatility.

Result: Consistent, predictable payments of $66,000 year after year until life expectancy, reducing risk and enhancing spending confidence. Even after life expectancy, the retiree receives income from both the Age Pension and the lifetime income product. This contrast shows how fragmented management of the three core pillars of retirement income often leads to less reliable outcomes compared to coordinated, proactive solutions.

The game-changer: a single retirement paycheck

Imagine your super fund taking charge: handling Age Pension applications, fine-tuning drawdowns across products and, over time, delivering a single, flat, inflation-protected paycheck that feels like your working salary. This automates compliance, maximises consumption efficiency and social security entitlements, and reduces volatility, empowering retirees to spend with greater certainty.

Not only that, but a retirement paycheck could also enhance the power of Retirement Estimates issued under ASIC rules, with the potential to replace the current generic account-based pension only projections that assume theoretical drawdowns with accurate, personalised forecasts that incorporate lifetime income and actual expected dynamic drawdown adjustments. This would improve accuracy, engagement, and trust – aligning with evolving best practices and supporting better planning in a changing system.

In fairness, delivering the retirement paycheck requires the orchestration of several activities across a fund, including the administration of retirement income sources, and access to data for Age Pension purposes is a key dependency, no doubt. However, none of these challenges are insurmountable.

As super funds innovate under regulatory encouragement, and to support distribution functions, the retirement paycheck emerges as the critical missing piece. It's time to close the gap between trustee-designed ideals and everyday reality. What challenges have you encountered with implementing the retirement paycheck and what support do you need to make this a reality? Share your thoughts below!